Barons of Banking (Glimpes of Indian Banking History)

Book Specification

| Item Code: | NAG528 |

| Author: | Bakhtiar K. Dadabhoy |

| Publisher: | Random House India |

| Language: | English |

| Edition: | 2013 |

| ISBN: | 9788184003499 |

| Pages: | 528 (53 B/W and color illustration) |

| Cover: | Hardcover |

| Other Details | 9.5 inch x 6.0 inch |

| Weight | 910 gm |

Book Description

Barons of Banking highlights the contributions of six distinguished personalities from the world of banking-Sir Sorabji Pochkhanawala, Sir Purshotamdas Thakurdas, Sir Chintaman D. Deshmukh, A.D. Shroff, H.T. Parekh, and RK Talwar-who not only played a pioneering role in the growth of the institutions which they founded, or were actively associated with, but left an indelible mark on the banking industry as a whole. Through the narration of the history of five key institutions-the Central Bank of India; the Reserve Bank of India; the State Bank of India; the Industrial Credit and Investment Corporation of India Ltd; and the HOUSing Development and Finance Corporation Ltd-the author gives us a keen insight into the contributions of these luminaries to banking in India. Also included is a narration of the recommendations of important committees and commissions which influenced the course of Indian banking.

Divided into four parts, the book uses hitherto unused archival material recently put in the public domain by the RBI. Of particular interest is a discussion of the acrimonious relationship between Sir James Grigg, the Finance Member of the Viceroy's Executive Council and Sir Osborne Smith, the first Governor of the RBI, which throws fresh light on a spat which remains unprecedented not only in the bank's history, but possibly in all of banking history.

Meticulously researched and engagingly written, this book will be of interest to both the academic and general reader and, of course, to the professional banker interested in a selective peep into the history of his profession.

Bakhtiar k. Dadabhoy is a civil servant based in Mumbai. He was educated at Hindu College, Delhi University, and at the Delhi School of Economics. He is the author of five books including the best-selling Jeh: A Life of JRD Tata and Sugar in Milk: Lives of Eminent Parsis. Dadabhoy also contributes articles to newspapers and magazines. He did a daily column 'This Day in History' for the Hindustan Times and HT Next for five years. His other interests include painting and quizzing. He was on BBC's Mastermind India in 2000.

This book is not a history of the development of Indian banking during the last century, nor is it a collection of biographical profiles of the six personalities who figure prominently in it. However, in a sense it is a bit of both. The author offers us glimpses of Indian banking history intertwined expertly with the pioneering contributions of six eminent personalities whose stellar contributions transcended the boundaries of individual institutions and influenced the banking industry as a whole.

When the trustees of The A.D. Shroff Memorial Trust invited Bakhtiar K. Dadabhoy to author this book they had two objectives in mind. First, to identify and narrate some of the seminal events and episodes which shaped the course of Indian banking; and second, to recognise and highlight the contributions of six illustrious individuals who made a crucial difference. Bakhtiar has accomplished this task admirably. A book such as this with its emphasis on facts could easily have become a dreary catalogue of dry statistics and facts but the author enlivens his narrative with colourful details and interesting anecdotes, and deserves to be congratulated for his diligent and resourceful research. This book, focusing as it does on the history of five institutions whose importance is indisputable, provides a broad-brush tapestry of some of the seminal events and institutions which shaped Indian banking. Delicately woven into this fabric are the contributions of six illustrious individuals whose contribution to Indian banking was immense.

The great historian Arnold J. Toynbee has shown that the great civilizations of the world evolved as a result of the forceful response provided by the inhabitants of a region when faced with a massive challenge posed by a changing environment. Thus the Egyptian civilisation evolved when a prolonged drought forced the inhabitants of the region to enter and drain the dangerous marshes of the Nile delta to create the fertile Nile valley. Economic systems and financial institutions are no different. The evolution of the Indian banking system and the creation of its major financial institutions can equally be traced to the responses provided to emerging challenges. And, in these responses the 'barons' of this banking history played a leading role.

When Sir Sorabji Pochkhanawala incorporated the Central Bank of India, he did not merely start a new bank. In an era of foreign domination, and in the teeth of much opposition, he demonstrated that a bank owned and managed by Indians could successfully compete with, and even outperform, many of the existing banks which were under foreign management. In paving the way for many others to follow he laid the foundation of the Indian commercial banking system.

Sir Chintaman D. Deshmukh, the first Indian Governor of the Reserve Bank of India and Sir Purshotamdas Thakurdas, its most forceful and longest serving founder-director, fought courageously and tenaciously to preserve the autonomy of the bank, an autonomy which it enjoys to this day. In this context it is interesting that in writing about Sir Osborne A. Smith, the first Governor, the author revisits the early years of the Reserve Bank of India using the recently released papers of the second Governor, Sir James Taylor.

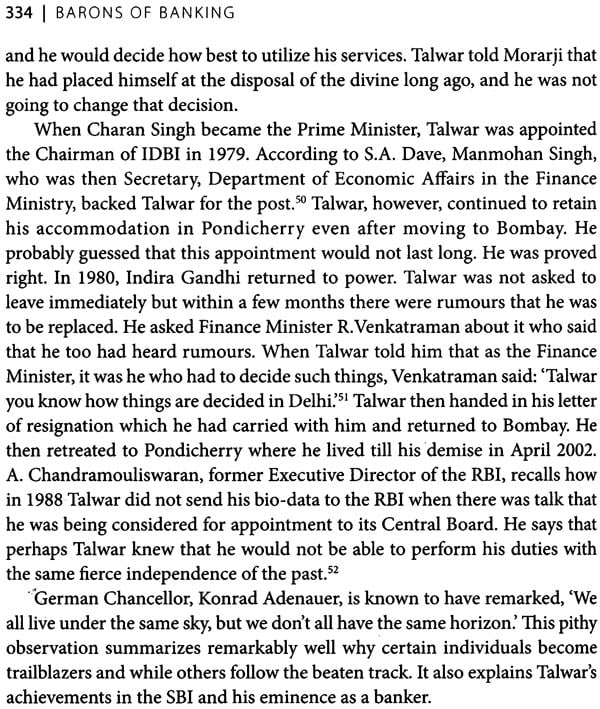

A.D. Shroff was the colossus who straddled many fields in the financial world whether it was banking, insurance, finance or economic policy. While he played a stellar role in the conception and establishment of some of the most important institutions in the banking sector, perhaps his most memorable contribution was as one of the representatives at the Bretton Woods Conference where his passionate appeal on India's behalf established India's credentials as a force to be reckoned with on the global financial stage.

R.K. Talwar of the State Bank of India was the legendary commercial banker who in the emerging era of nationalized banking demonstrated an admirable professional independence which made him a role model for all his successors. Finally, there is H.T. Parekh, the ultimate visionary and institution- builder, who not only widened the boundaries of development banks but who is rightly acknowledged as the father of housing finance in the country.

These then are the personalities who adorn the pages of this book. They were innovators, executors and consolidators. They were all men of extraordinary integrity, courage and conviction, and as the pages of this book will show, national interest informed their every action. The Indian banking system which they helped shape has stood the test of time, and the resilience with which it has withstood the challenges posed by several global crises over the last two decades is evidence of its robustness.

This book is as much a tribute to the Indian banking system as it is to the six 'barons' who occupy a place of pre-eminence in it.

While this book revolves around the history of five banking institutions and the role played by six eminent banking personalities in the twentieth century, it will be useful to first briefly trace the history of banking in Indi.

A BRIEF HISTORY OF BANKING IN INDIA The year 1860, or one of its close neighbours, marks a watershed not only in the political sphere but also in the economic and financial fields. In the latte: the watershed is marked by the introduction of Railways and factory industry in the mid 1850s, by James Wilson's reform of the Central Government' finances in the early 1860s, and by the extension of the principle of limited liability to banking.

In 1860, western-type financial institutions were limited to about a half dozen commercial banks which coexisted with hundreds of indigenous banks and thousands of rural moneylenders. The British applied the term indigenous bankers to all kinds of private bankers, moneylenders, banking or money lending firms, with the distinction that the 'banker' in addition to making loans, received deposits and dealt in hundis. The moneylender, on the other hand, only advanced loans and did not usually receive deposit or deal in hundis. Indigenous banking remained confined to certain caste principally the Vaishyas and Jains, both spread all over the country; the Chettis of Madras; the Marwaris of Rajputana and Central India; the Shikarpuris and Multanis of Sind and Bombay; the Bohras of Gujarat; and Khatris of Punjab The indigenous bankers were of three variants: those whose entire business was banking; those whose principal business was trading but who employee surplus funds in banking; and those who divided their funds equally between banking and trading.

The bankers had, however, created at least one important type of financial instrument, the hundi, which is similar to a bill of exchange and was used as means of short-term financing as well as for the inter-local transfer of funds. 'The hundi handed down for centuries from an unrecorded past must ever remain a singular monument to the financial acumen and ingenuity of these bankers'). The hundi, still used today, is an unconditional order in writing by one person on another for payment on demand or after the specified time of a certain sum of money, to a person named therein. It has no legal status but unlike the bill of exchange, it can be used for raising or remitting funds without reference to any particular trade transaction.

Hundis are of two types: demand, darshani; and usance, muddati. The former is payable on demand while the latter is payable after expiry of the stipulated period. The hundis are also dhanijog or sahjog. In cashing the latter, a banker has to ensure that the presenter is the proper person entitled to payment, but he is free from this responsibility in cashing the former. Two other types of hundis are farmanjog which are payable on demand and jokhami which are drawn against goods dispatched and contain certain conditions in accordance with which if goods are lost or destroyed in transit, the drawer or holder of the hundi has to suffer the loss. Payment of such hundis is made on safe receipt of the goods and their purchaser acts as a sort of insurance agent.

The hundi system worked well and dishonouring a hundi was a rare event with a social stigma attached to it. Bankruptcy was a public event marked by lighting a lamp for all to see. The system worked on mutual trust and confidence. It is said that the Jain brothers drew a hundi for no crores on the Nagar Seth, the 'City Banker' of Ahmedabad for building the Dilwara temples on Mount Abu. Ruling princes also paid loans or tributes by means of hundis on their bankers. In 1666, Shivaji borrowed 66,OOO from Kumar Ram Singh, son of Raja Sawai Iaisingh I of Jaipur, and gave a hundi on his officers in the Deccan to pay the Raja.

Of all the banking houses of India, ancient or modern, none has achieved a place in history comparable with the house of Jagat Seths whose transactions were on an enormous scale. The founder of the house was Hiranand Sahu who migrated from Jodhpur to Patna in 1652. He was succeeded by his son Manikchand in 1711 who made a loan of 1 crore to aid the revolt of Farrukhsiyar and was rewarded by him with the title of Nagar Seth. Manikchand was succeeded in 1714 by his nephew and adopted son, Fateh Chand, under whom the house reached new heights of glory and power. In 1722, the emperor Mahmud Shah conferred on Fateh Chand the title of Jagat Seth as a hereditary distinction. The height of the prosperity of the house was attained at the time of Mahtab Rai and his brother, the two grandsons of Fateh Chand. They, however, paid the price for playing politics and were executed by Mir Kasim.

Benares was the original home of many banking houses. Pre-eminent among them during the latter half of the eighteenth century was the house of Gopaldas Sahu and his son Manohar Das. There was hardly a place of importance in the country which did not have an accredited agent of the house. Gopaldas was the East India Company's farmer of revenues and treasurer at Benares. Contemporary with Gopaldas was Trawadi Arjunji Nathji of Surat, a Nagar Brahmin hailing from Benares, who was reputed to be the richest banker in Gujarat. He was officially proclaimed as the 'Company's Shroff in India. Many years before Arjunji Nathji there flourished in Surat (1619-1634) the famous merchant banker Virji Vora described in the East India Company's correspondence and travellers' notes as 'prime merchant of this town (Surat), 'the greatest and richest general merchant that inhibited the vast kingdom' with resources oH80 lakhs. Ahmedabad had its Seth Shantidas whose family in later times was more widely known by the title of Nagar Seth, conferred on it by either Shah [ahan or Aurangazeb.

The local Chettis were prominent in the South for their banking activities. However, Gujarati merchants and bankers also appear to have been active and in 1740 the largest banking house of the South was that of Bukanji Kasidas, a Gujarati, who was styled as 'Sarkar's sowkar and the chief shroff of the province'.

Modern Indian Banking Banking on modern lines began in India with the foundation of the agency houses of Calcutta and Bombay in the eighteenth and early part of the nineteenth centuries. As the East India Company's trading and administration grew, British merchants progressively took over some of the internal, and a large part of the external trade. The financing of trade, the British army and civil personnel's need to remit savings back home, and facilities for the new administration to remit its revenues from districts to head offices, all required a modern banking system.

The financial needs of the Company and the British community were met by the managing agency houses-trading concerns initially interested mainly in tea and indigo. Later, they diversified into a wide variety of fields becoming the earliest example of a modern conglomerate. The agency houses extended their business to include banking which soon became the most important adjunct to their business. The fortunes they made gave them the name of merchant princes of India, while the money they and the Company servants made was called 'shaking the Pagoda Tree? The Company's services were the main recruiting ground and many enterprising men set up independent businesses after leaving the employment of the Company and amassed large fortunes. As S.K. Muranjan observed, 'Many of them were men who abjured the limited prospects of the Company's employment for the incalculable prizes of private trade and commerce.

Although some of the later joint-stock banks rose independently of agency houses, these must be regarded as pioneers in this field. All banks, except one, were started on the basis of unlimited liability. The agency houses had no capital of their own and depended upon deposits for their funds. They financed the movement of crops, issued paper money, and paved the way for the establishment of joint-stock banks, the earliest of which was the Bank of Hindustan established in 1770 by Alexander and Co. The bank was wound up in 1832 when its parent agency failed. Since the agency houses had little capital of their own, and did not possess knowledge of modern European or conventional Indian banking, the vicissitudes and trade crises that visited their agency businesses were wholly transmitted to their banking activities. Thus when an agency house failed, so did its bank. The Calcutta Bank established by Palmer and Co., perished when its agency house failed. However, due to the Company's opposition to starting a bank, it was left to the managing agencies to fill the void. 'The immediate and perhaps the most outstanding and permanent achievement of these banks was the introduction of a note circulation in this country.

The Bengal Bank and the General Bank of India were established around 1785. The former failed in 1791 owing largely to the panic of war with Tipu Sultan. The latter was voluntarily liquidated in 1793 when it failed to earn profits. These banks were chartered by the East India Company and were followed by banks established under Acts of the Indian Legislature. The latter may be divided into two groups, the first consisting of the three Presidency Banks, and the second, the Indian joint-stock banks. By 1829-30 'the Agency Houses had stumbled into their final crisis," Among those that failed were Alexander and Co., Colin and Co., Fergusson and Co., Palmer and Co., and Mackintosh and Co. Seven or eight of these alone were reported to have lost £15 million and with them were dragged into insolvency the associated banks as well. Between this crisis and 1860, only twelve banks were launched (all with European management), half of which failed. Some were mere frauds and others failed due to imprudent investment in industries.

The Presidency Banks The most important institutional gain of this period was the emergence of the three Presidency banks destined to play an important role in Indian banking. From the early days of banking, there was a vision of one great 'State Bank' or 'General Bank' and many of the joint-stock banks which were set up were frequently inspired by such ideas. The need for establishing a modern bank was felt during the reign of Charles II, when a decision was taken in 1683 and conveyed to the Company in Madras to raise capital and accept deposits from the public. However, nothing came of it. Next, the Government Bank of Bombay was set up in December 1720 and closed in 1770. In 1773, Warren Hastings revived the idea and started the General Bank of Bengal and Bahar but this was aborted by some of his colleagues. The Court of Directors reiterated their opposition in 1787 by prohibiting the Indian government from extending their support to banking institutions. It was only in 1806 that the government resolved to support the Accountant General of Bengal, Henry St George Tucker's scheme, and recommended the establishment of a bank in Calcutta in which the government was to have the power of nominating the Directors and hold a large part of the share capital as well.

The Company, while objecting to the principle of government becoming a partner, acquiesced, and the Bank of Calcutta was set up on May 1,1860, with a capital of 50 lakhs, one- fifth of which was contributed by the government. It received its charter in 1809 and became the Bank of Bengal. The Company contributed one-fifth of the capital and obtained the right to appoint three Directors. The bank was entrusted with government funds and its notes alone were recognized by government, but it was not entrusted with the remittance of revenues from the mofussil. Its charter was reviewed in 1823 when its note issue was revised to 2 crores and cash reserve requirements lowered to one- fourth of the outstanding liability. In 1839, it was allowed to open branches and to deal in inland but not foreign exchange.

The Bank of Bombay was established in 1840 with a share capital of 52.1S lakhs. The Company held 3Iakhs. The Bank of Bombay was involved in the wild speculation of 1862-65 that followed the American Civil War and the rise in the price of cotton. It suffered serious losses and went into liquidation in 1868. Although the depositors were repaid fully, the shareholders lost nearly all their capital. However, almost immediately a new bank with the same name and a capital of 1 crore, (with 50 lakhs being paid-up), was formed. The Bank of Madras was incorporated in 1843 with a share capital of 30 lakhs. The Company, as in the case of the Bank of Bombay, held shares of lakh.

Prior to 1862, the Presidency Banks were directly controlled by government and had to work within certain restrictions imposed on them by their charters. They enjoyed the valuable right of note issue. In 1862, they were deprived of this right although they continued to manage the new government note issue as agents of the government. As compensation, they were freed from many of the old restrictions on business, and were given the use and management of government balances. But the danger of such relaxation became evident when the Bank of Bombay failed. Negligence, incompetence, abuse of powers, and absence of sound legal advice all played a role, but as the Bank of Bombay Commission which inquired into the lamentable episode observed, the removal of restrictions opened the door to 'great laxity of practice and a ruinous system of banking.

The Presidency Act of 1876 restored substantially the old restrictions upon all three banks to safeguard the interests of government and the public. It prohibited the banks from conducting foreign exchange business. Lending for a period longer than six months, or upon mortgage, or on the security of immovable property was also forbidden. The government balances at the disposal of the banks were strictly limited. The government sold its shares in the banks and ceased to appoint official Directors. In return, most government banking work was retained in their hands and the prestige that this gave them enabled them to secure a large amount of other banking business.

While the Presidency Banks established branches at many important trade centres, they lacked points of contact, a fact which was often deplored. It was strongly felt that there should be only one bank of this kind for the whole country. In 1867, G. Dickson, the Secretary and Treasurer of the Bank of Bengal, placed before the government a proposal for the amalgamation of the three banks. His proposal did not find favour on the grounds that such an institution might overshadow the government itself. It was also thought that it would be difficult to manage, and that the merchants of the other two trading centres i.e. Bombay and Madras were entitled to separate banks to promote their own interests and convenience. In 1898, some witnesses before the Fowler Committee advocated the establishment of a central bank but the government did not favour the proposal. The Presidency Banks themselves wanted to retain their individuality and opposed amalgamation. It was the banking crisis of 1913-17 and the experience of the First World War during which they cooperated informally, but profitably, coupled with the fear of an invasion from London banking interests, which gave the Presidency Banks a keener realization of the commonness of their interests. They amalgamated to form the Imperial Bank of India in 1921.

| Acknowledgement | ix | |

| Message | xvii | |

| Foreword | xix | |

| Introduction | xxiii | |

| Book I | ||

| The Central Bank of India | ||

| Prologue | 5 | |

| 1 | A leap of faith | 10 |

| 2 | Weathering the storm | 19 |

| 3 | Consolidation and expansion | 28 |

| 4 | Innovations and Ideas | 38 |

| 5 | This unifortunate matter' | 47 |

| Book II | ||

| Central Banking in India | ||

| Prologue | 63 | |

| Part I | ||

| Indian Currency and Finance | ||

| 6 | The exchange ratio | 79 |

| 7 | The hilton young commission | 84 |

| 8 | Minute of dissent | 94 |

| 9 | Government's little gain, people's great loss | 102 |

| 10 | Banking reforms | 108 |

| 11 | Deliberations at the round table conferences | 117 |

| Part II | ||

| The Reserve Bank of India | ||

| 12 | Central Banking in India: The beginnings | 127 |

| 13 | The politics of monetary autonomy | 134 |

| 14 | A reserve bank at last | 145 |

| 15 | Sir osborne arkell smith: The saga of the first RBI governor' | 152 |

| 16 | Driving force, restraining influence' | 174 |

| 17 | An indian governor | 179 |

| 18 | Central banking: The war years | 189 |

| 19 | Towards a new monetary order | 201 |

| 20 | The Bretton woods conference and after | 215 |

| 21 | The sterling balances | 230 |

| 22 | Nationalization of the reserve bank of India | 242 |

| Book III | ||

| The State Bank of India | ||

| Prologue | 253 | |

| 23 | The presidency banks | 257 |

| 24 | The imperial bank of India | 272 |

| 25 | From imperial bank to state bank | 283 |

| 26 | In the public sector | 294 |

| 27 | The talwar years, 1969-1976 | 309 |

| Book IV | ||

| Development Banking | ||

| Prologue | 339 | |

| 28 | The shroff committee report | 351 |

| 29 | The making of a development bank | 367 |

| 30 | The maturing of a development bank | 383 |

| 31 | A House for All: H.T. Parekh and HDFC Limited | 404 |

| Notes | 425 | |

| Bibliography | 460 | |

| Index | 465 | |

| A Note on the type | 479 |